|

M |

anaging your money involves choices and decisions. An important decision in

how you manage your money is what to do about credit. For many people, using

credit becomes a critical part of their money management system. For most of us, credit is the one financial tool that has allowed us to buy homes, cars, and other “big ticket” items.

![]()

Use the 10 percent rule. Your debt load (except for your home mortgage) should not exceed 10 percent of your yearly after-tax income.

![]()

Credit is also used for buying other products or services, such as travel. Some people use credit when they don’t have the cash on hand for emergencies such as car problems. Indeed, there are people who use credit for nearly all their purchases, from food to fun to furniture. Using credit is convenient. It eliminates the need to carry large amounts of cash, and provides a record of purchases. These features can give you flexibility in deciding how to manage your money.

A Member of the University of Maine System

There also are some risks with using credit. Credit, or the use of it, is a promise to pay later, usually with interest, for something you buy now. If you are not careful, you can get into debt quickly. Use of credit can lead to overspending. Credit expenses can be costly and tie up money you might want to use on something else. Unwise use of credit may also lead to bad credit ratings and affect future credit-based purchases.

Can you afford more debt?

You want to buy a freezer, but you don’t have the cash to pay for it. Can you afford to borrow the money? How do you decide?

Use the 10 percent rule. Your debt load (except for your home mortgage) should not exceed 10 percent of your yearly after-tax income.

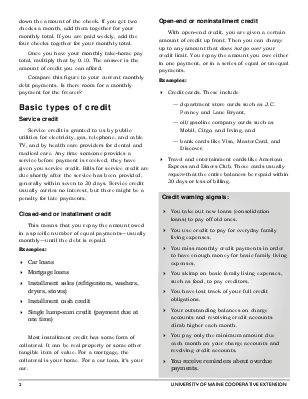

Write down how much money you bring home each month. If you get one check a month, write

|

Example: $1000 x .10 = $100 1. Enter your monthly take-home pay: $_________ 2. Multiply by 10 percent x 0.10 = _________

3. Amount of monthly credit you can afford $ _________ 4. Compare your current monthly debt $ _________ |

down the amount of the check. If you get two checks a month, add them together for your monthly total. If you are paid weekly, add the four checks together for your monthly total.

Once you have your monthly take-home pay total, multiply that by 0.10. The answer is the amount of credit you can afford.

Compare this figure to your current monthly debt payments. Is there room for a monthly payment for the freezer?

Service credit is granted to us by public utilities for electricity, gas, telephone, and cable TV, and by health care providers for dental and medical care. Any time someone provides a service before payment is received, they have given you service credit. Bills for service credit are due shortly after the service has been provided, generally within seven to 30 days. Service credit usually carries no interest, but there might be a penalty for late payments.

This means that you repay the amount owed in a specific number of equal payments—usually monthly—until the debt is repaid.

Examples:

Car loans

Mortgage loans

Installment sales (refrigerators, washers, dryers, stoves)

Installment cash credit

Single lump-sum credit (payment due at one time)

Most installment credit has some form of collateral. It can be real property or some other tangible item of value. For a mortgage, the collateral is your home. For a car loan, it’s your car.

With open-end credit, you are given a certain amount of credit up front. Then you can charge up to any amount that does not go over your credit limit. You repay the amount you owe either in one payment, or in a series of equal or unequal payments.

Examples:

Credit cards. These include

— department store cards such as J.C. Penney and Lane Bryant,

— oil/gasoline company cards such as

Mobil, Citgo, and Irving, and

— bank cards like Visa, MasterCard, and Discover.

Travel and entertainment cards like American Express and Diners Club. These cards usually require that the entire balances be repaid within 30 days or less of billing.

Уважаемый посетитель!

Чтобы распечатать файл, скачайте его (в формате Word).

Ссылка на скачивание - внизу страницы.